How to Budget for a Major Roof Repair: A Strategic Homeowner’s Blueprint

As homeowners and business owners in Fort Lauderdale, Hollywood, and across South Florida, we understand that a major roof repair isn’t just an expense – it’s a critical investment in your property’s safety, value, and structural integrity. Especially in our unique climate, where intense sun, humidity, and the ever-present threat of hurricanes dictate specific needs, a strategic approach to budgeting is not just smart; it’s essential.

At Shieldline Roofing, we believe in empowering our clients with the knowledge to make informed decisions. This blueprint will guide you through the financial preparedness and tactical execution required for a major roof repair, ensuring your investment stands strong against the elements for years to come.

Key Takeaways:

- Proactive Planning is Paramount: Establish a dedicated maintenance fund and schedule regular inspections to avert costly emergencies.

- Comprehensive Cost Analysis: Obtain multiple, detailed quotes and factor in all potential hidden expenses, understanding regional cost variances specific to South Florida.

- Strategic Financing Options: Explore diverse funding avenues, from home equity to emergency loans, to secure the best financial solution for your situation.

- Timing is Tactical: Execute repairs at optimal times to leverage weather conditions, contractor availability, and prevent escalating damage in our challenging environment.

1. Assessing the Scope: A Strategic Reconnaissance for South Florida Properties

Before any budgeting begins, a clear understanding of the repair’s magnitude is essential. A “GEO Strategist” approaches this by understanding the terrain (your roof) and the forces at play (weather, material degradation). For properties in Fort Lauderdale, Hollywood, and surrounding areas, this means considering the **High-Velocity Hurricane Zone (HVHZ)** requirements and the relentless impact of our tropical climate.

Professional Inspection: Your Indispensable First Step

The indispensable first step is a professional inspection. A certified roofing professional, intimately familiar with the **Florida Building Code (FBC)** and local conditions, provides an objective assessment of damage. They can identify structural issues often hidden from the untrained eye, especially critical after a storm or for older South Florida homes that may not meet current code.

Identifying Damage Types: Beyond the Obvious

Differentiate between routine wear-and-tear (accelerated by our intense sun), storm-induced damage (wind uplift, hail, debris impact common during hurricane season), and deeper structural compromises. This informs repair urgency and potential insurance claims. In South Florida, even minor leaks can quickly lead to extensive mold and wood rot due to high humidity, escalating repair needs rapidly.

Material Considerations & Regional Impact: Built for Florida

Understand the specific material of your roof (e.g., asphalt shingles, metal, concrete tile, clay tile, or flat roof systems like TPO or Modified Bitumen). Material costs, availability, and labor rates can vary significantly by geographic region in Florida, impacting the overall budget. For instance, tiles are popular here for their durability and aesthetic, but installation requires specific expertise and adherence to **FBC wind-load requirements**.

Hidden Vulnerabilities: Planning for the Unseen

Beyond visible damage, strategize for potential underlying issues like damaged decking (often compromised by water intrusion), compromised insulation (leading to higher energy bills in our heat), or ventilation problems (which can trap heat and humidity, degrading your roof from within). Shieldline Roofing’s inspections delve deep to uncover these often-costly surprises.

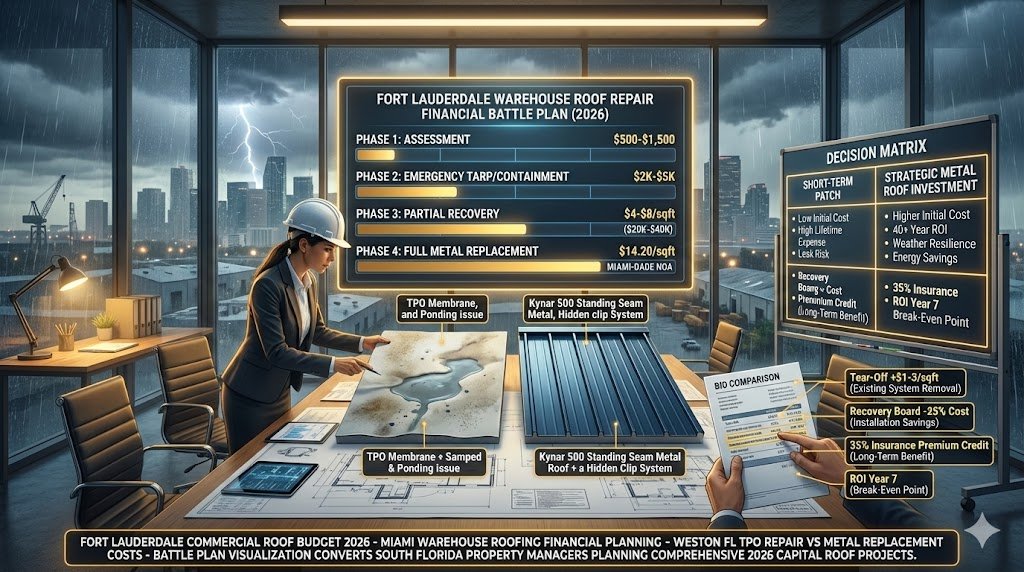

2. Devising the Budget: A Financial Battle Plan for Your Fort Lauderdale Roof

Once the scope is clear, crafting a robust financial plan is crucial. A strategic budget anticipates not just immediate costs but future contingencies, especially vital for meeting **Florida Building Code (FBC)** compliance.

Obtaining Multiple Quotes: Informed Decisions

Solicit at least three detailed bids from licensed and insured contractors who specialize in South Florida roofing. This provides a competitive baseline and insight into different approaches, allowing you to compare not just price, but also proposed materials, warranties, and adherence to local regulations.

Breaking Down the Estimates: Scrutinizing Every Line Item

Scrutinize quotes for line items covering materials (e.g., specifying **FBC-approved underlayment** and **fasteners**), labor, **permits (which are mandatory for major repairs in Fort Lauderdale and Hollywood)**, waste disposal, and potential unforeseen expenses like replacing damaged sheathing or addressing mold. A transparent quote from Shieldline Roofing will detail these components clearly.

[STAT]: The average cost for a major roof repair or replacement in the U.S. ranges from $8,000 to $15,000, with significant regional variations up to $25,000 for premium materials or complex projects in high-cost areas. In South Florida, these costs can often trend towards the higher end due to specialized materials, strict building codes, and labor demands, particularly after storm seasons.

Contingency Fund Allocation: Preparing for the Unpredictable

Always factor in a contingency of 10-20% above the highest estimate. Unexpected issues are common in major repairs, especially in older homes or after hidden water damage is uncovered. A strategist prepares for the unpredictable, ensuring your project stays on track without last-minute financial stress.

Factors Influencing Cost: South Florida Specifics

- Roof Pitch & Accessibility: Steeper roofs and challenging access (e.g., multi-story buildings) increase labor costs due to specialized safety equipment and extended work times.

- Square Footage: The larger the roof, the higher the material and labor expenditure.

- Material Choice: Premium materials with higher **wind-resistance ratings** (e.g., **Class 4 Impact Resistance**) command higher prices but offer superior longevity and storm protection crucial for our region.

- Permit Fees: Local regulations in Fort Lauderdale and Hollywood dictate permit requirements and associated costs, which are essential for ensuring your roof meets **Florida Building Code** standards.

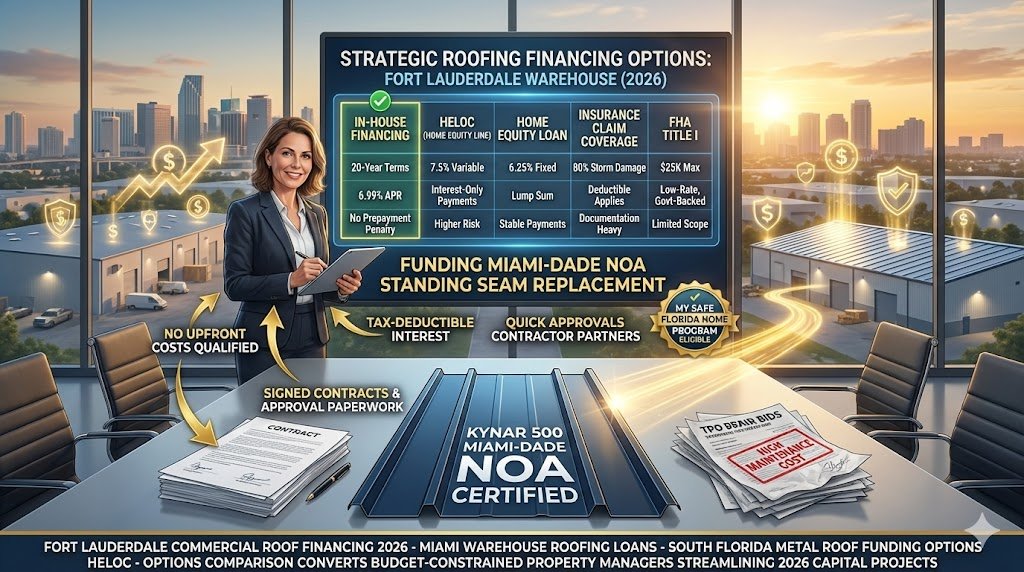

3. Strategic Funding & Financing Options: Securing Your Resources

A geo strategist knows that resources must be marshaled effectively. This means exploring all available funding avenues and choosing the most advantageous for your specific needs in South Florida.

Dedicated Home Maintenance Fund: The Ideal Scenario

The most financially prudent approach is to have a pre-existing fund. Regularly contributing to a specific account for home repairs mitigates the impact of large, unexpected expenses. This proactive saving is your best defense against major surprises.

Home Equity Loans or Lines of Credit (HELOC): Leveraging Your Investment

Leveraging your home’s equity can provide competitive interest rates, making it a popular choice for significant repairs. For many South Florida homeowners, their property is their most valuable asset, and a HELOC can provide the necessary capital with favorable terms.

Personal Loans: Quick Access, Higher Rates

While typically carrying higher interest rates than secured loans, personal loans offer quicker access to funds and require no collateral. This can be a viable option for those needing immediate repairs without access to home equity.

Contractor Financing: Convenient Solutions from Shieldline Roofing

Many reputable roofing companies, including Shieldline Roofing, offer in-house financing plans to help spread the cost. Evaluate interest rates and terms carefully against other options to ensure it’s the best fit for your budget.

Insurance Claims: Your Ally Against Storm Damage

If damage is due to sudden, unexpected events like storms (e.g., a hurricane, high winds, or hail) or fires, your homeowner’s insurance policy may cover a substantial portion of the repair cost. Document everything meticulously – photos, dates, and detailed reports. Shieldline Roofing has extensive experience assisting homeowners in Fort Lauderdale and Hollywood with their insurance claims processes, ensuring proper documentation and maximum coverage for **FBC-compliant repairs**.

Government or Local Programs: Exploring Assistance

Research if any local, state, or federal programs offer assistance for specific home improvement projects, especially for energy efficiency upgrades (which a new roof can contribute to) or low-income homeowners. While less common for routine repairs, these can be valuable resources.

4. Timelines & Tactical Execution: Preventing Cost Overruns in South Florida

Strategic timing can significantly impact both the cost and effectiveness of a major roof repair, especially when navigating South Florida’s unique weather patterns and contractor availability.

Optimal Repair Seasons: Beat the Rush

Scheduling repairs during mild weather conditions (typically spring or fall) can lead to better workmanship, faster completion, and potentially lower labor costs as contractors aren’t rushing in peak emergency season. Crucially, aim to complete major repairs **before hurricane season (June 1st to November 30th)** to ensure your property is prepared for severe weather.

The Cost of Delay: A Rapid Escalation

Procrastinating on major repairs invariably leads to exacerbated damage, impacting structural integrity and increasing the eventual financial burden. In South Florida’s high humidity, a minor leak can quickly become a major mold infestation or structural rot, requiring more extensive and expensive remediation.

[STAT]: Delaying minor roof repairs can increase the total project cost by an estimated 15-20% annually due to exacerbated damage and secondary structural issues like water intrusion and mold growth. This percentage can be even higher in a climate like ours.

Scheduling & Contractor Availability: Strategic Planning Pays Off

Strategic planning allows you to book reputable contractors like Shieldline Roofing during their less busy periods, potentially securing better rates and more focused attention on your project. Trying to find a quality roofer right after a hurricane can be challenging and costly due to demand surges.

Property Value & Resale Implications: Protect Your Investment

A damaged roof can significantly detract from property value and complicate sales. Buyers in South Florida are highly aware of roof condition due to insurance requirements and hurricane concerns. A timely, **FBC-compliant** repair or replacement preserves asset value and provides peace of mind for future homeowners.

FAQs for Fort Lauderdale & Hollywood Homeowners

How often should my roof be inspected in South Florida?

It’s recommended to have your roof professionally inspected at least once a year, ideally in the spring before hurricane season, and immediately after any severe weather events. For homeowners in Fort Lauderdale and Hollywood, this proactive approach is crucial for early detection of issues exacerbated by sun, wind, and rain.

Can I do a partial roof repair, or do I need a full replacement?

This depends entirely on the extent, age, and nature of the damage. Minor, localized damage may only require a partial repair, especially on newer roofs. However, widespread damage, significant age (e.g., asphalt shingles over 15-20 years old), or structural issues often necessitate a full replacement for long-term safety, **Florida Building Code compliance**, and cost-effectiveness. Your Shieldline Roofing inspector can provide a detailed assessment and recommendation.

What are the key signs my roof needs major repair in our climate?

Common signs in our South Florida climate include missing or broken shingles/tiles (especially after wind events), granules in gutters, water stains on ceilings or walls, sagging roof deck, visible light in your attic, and widespread moss or algae growth (indicating moisture retention). Any signs of **water intrusion** demand immediate attention to prevent mold and structural damage.

Will my home insurance cover the repair?

Homeowner’s insurance typically covers roof damage caused by sudden and unexpected events (e.g., hail, wind, fire, falling trees). It generally does not cover damage from neglect, wear-and-tear, or poor maintenance. It’s crucial to review your specific policy, understand your deductible, and file claims promptly if applicable. Shieldline Roofing can help you document damage accurately for your insurance company.

How do I choose a reputable roofing contractor in Fort Lauderdale or Hollywood?

Look for **licensed and insured contractors** with strong local references. Check their online reviews, ask for proof of insurance and licensing, get multiple written estimates detailing **FBC compliance**, and ensure they offer a warranty on both materials and labor. Avoid contractors who pressure you, demand full payment upfront, or appear immediately after a storm without proper local credentials. Shieldline Roofing prides itself on transparency, local expertise, and superior workmanship.

Protecting your home or business in South Florida starts with a strong roof and a smart financial plan. Don’t let a major repair become an overwhelming burden. For a complimentary, detailed roof assessment and estimate that factors in **Florida Building Code (FBC)** requirements and **HVHZ** specifics, contact Shieldline Roofing today. We are your trusted experts for Fort Lauderdale, Hollywood, and all of South Florida, dedicated to providing durable, code-compliant, and long-lasting roofing solutions.